The Numbers That Should Change How You Trade

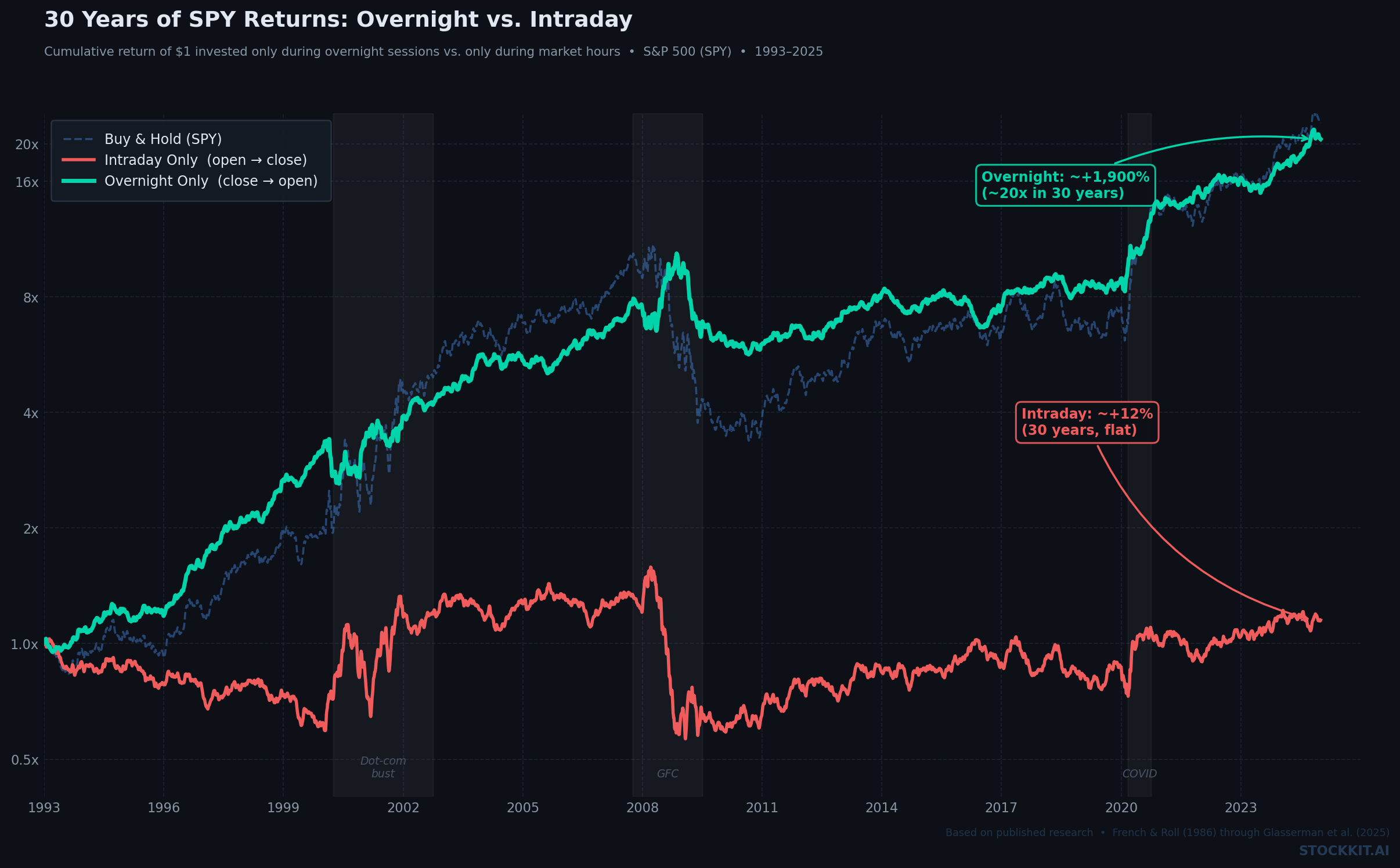

Over the past 30+ years, the S&P 500 has increased roughly 20-fold on a buy-and-hold basis. Break that return into two buckets — gains made from open to close (intraday) vs. gains made from close to the next day's open (overnight) — and what you find is striking.

Intraday returns over that 30-year span are barely positive, up only about 12% in total. The overnight strategy, by contrast, tracks almost identically to the full buy-and-hold return — up close to 20-fold.

Let that sink in. Thirty years of intraday trading: +12%. Thirty years of just holding overnight: nearly +2,000%.

This isn't a fringe observation. Over at least the past 30 years, nearly all gains in the U.S. stock market have been earned overnight, while average intraday returns have been negative or flat — a finding replicated across dozens of academic studies, including research from Yale, the London School of Economics, and the New York Federal Reserve.

This Isn't New — Researchers Have Known for Decades

The overnight effect was first formally documented by Ken French and Richard Roll back in 1986. It has been confirmed repeatedly since, across different time periods, different markets, and different methodologies.

The overnight effect is observed across most major equity markets and is consistent back to the 1990s at least. And yet just a smattering of papers over the years have explored this phenomenon — a tiny fraction of the attention devoted to other potential market anomalies such as momentum or value — leaving the overnight effect an overlooked and largely unexplained anomaly in financial markets research.

Think about that. One of the most persistent, most documented anomalies in all of finance gets almost no mainstream attention. Meanwhile, retail traders spend billions of hours and dollars trying to scalp intraday moves that, in aggregate, go nowhere.

Why Does This Happen?

The honest answer is that researchers are still debating the precise mechanism, but the leading explanations come down to risk pricing and market structure.

The Risk Premium Explanation

When the market closes, large institutional investors can no longer easily hedge their positions. They're exposed overnight to earnings releases, geopolitical events, economic data drops — all the things that move stocks the most. The theory is that overnight returns represent compensation for bearing that risk. You get paid a premium for holding when you can't easily get out.

The Market Structure Explanation

When markets first open, the first brokers willing to sell shares of high-demand stocks are smaller high-frequency trading firms. They have fewer assets and can accommodate fewer buyers — keeping the supply of in-demand stocks low and prices higher. The larger brokerage houses and asset management firms, which have more capacity, don't offer their supply until later in the morning. When they start selling, supply becomes plentiful and prices drop.

In other words, the morning open frequently represents a price peak driven by retail enthusiasm and thin supply — and the rest of the trading day is spent giving some of that back.

The News Cycle Explanation

A large part of the overnight return effect can be explained through features of intraday and overnight news. Earnings releases, analyst upgrades, FDA decisions, economic data — the highest-impact news almost always drops outside market hours. The price move happens at the open. By the time the average trader is reacting intraday, the opportunity has already passed.

What This Means for How You Trade

This data doesn't mean intraday trading is worthless. Plenty of traders profit intraday — but they're winning against other traders, not riding the market's underlying upward drift. It's a zero-sum game fought in the noisiest, most competitive hours of the day.

The overnight edge, by contrast, is structural. It's been there for 30+ years. It's tied to how markets are built, how risk is priced, and how information flows through the system.

Here's the practical takeaway:

1. Holding overnight is not reckless — it's historically where the returns live. The conventional retail wisdom is that holding overnight is dangerous. The data says the opposite: for quality stocks with real upward trends, holding through the close is how you capture the market's long-run gains.

2. The morning open is frequently the worst time to buy. If overnight demand has already run a stock up, the open price often reflects inflated enthusiasm. Buying into that volatility is swimming against the current — intraday returns on those positions will likely be flat or negative.

3. Your stock selection matters enormously. The overnight edge isn't uniform across all stocks. It's strongest in quality stocks with genuine upward trends — the kind that attract consistent institutional attention and get repriced positively overnight. Garbage stocks don't benefit from the overnight drift; they just gap down on bad news.

The RSI Connection: When the Overnight Edge Is Strongest

Knowing that stocks gain mostly overnight is useful. Knowing when a specific stock is about to enter its most powerful overnight-gaining phase is how you actually trade it.

That's where RSI comes in.

RSI (Relative Strength Index) measures momentum on a scale of 0–100. When a stock falls below RSI 30, it's considered technically oversold — meaning sellers have pushed it down to a point where it's trading at a discount relative to its recent history. That's when bargain hunters start moving in.

Here's what the charts show clearly: almost all significant gap-ups in a stock's price occur during the run from RSI 30 to RSI 70. That's the window when buyers are piling in, momentum is building, and the overnight repricing effect fires hardest. Institutions accumulating a position don't do it in one intraday session — they build over days, and a large portion of that price appreciation shows up at the open each morning as the stock grinds higher.

The opposite is equally true. When a stock crosses above RSI 70 into overbought territory and starts rolling back down toward RSI 30, the overnight gaps tend to reverse. Sellers are distributing, institutions are trimming, and the overnight drift that was working in your favor starts working against you.

This creates a remarkably clean strategic framework:

- RSI below 30 and turning up → You're at the starting line of the phase where overnight gains are most concentrated. This is when you want to be holding through the close.

- RSI between 30 and 70, trending up → You're in the heart of the move. Each overnight session is adding to the run.

- RSI approaching or above 70 → The most powerful phase of overnight gains is likely behind you on this cycle. Risk/reward starts shifting.

The beauty of this approach is that it puts probability firmly on your side. You're not guessing which direction a stock will move — you're identifying stocks that have already been sold down to a discount, are showing early signs of buyer interest, and have historically demonstrated that this is the exact phase where overnight gap-ups cluster.

How Stockkit Helps You Position for the Overnight Edge

The overnight edge is powerful, but it has a prerequisite: you need to be in the right stocks. A stock that's trending down doesn't benefit from overnight drift — it gaps down on news or gets sold at the open by institutions trimming positions.

Stockkit's Rockkit Rating is built around exactly this problem. It evaluates stocks across momentum, volume trends, and technical positioning to surface the ones that are statistically best positioned for overnight moves — including RSI positioning as a core signal. The alert system lets you know when those setups are forming, specifically when quality stocks are crossing up from oversold territory into the RSI 30–70 window where overnight gap-ups historically cluster.

You're not reacting to the move. You're positioned before it.

Frequently Asked Questions

Why do stocks gain more overnight than during the day?

The leading explanations involve risk premiums for holding when markets are closed, news cycles that release the highest-impact information overnight, and market structure dynamics where early morning demand outpaces supply. The effect has been documented consistently across 30+ years of U.S. market data.

Is the overnight stock strategy profitable for retail investors?

The broad overnight effect is real, but capturing it purely mechanically — buying the close and selling the open every day — is difficult due to transaction costs and execution friction. The smarter application is using the data to inform which stocks to hold and why holding through the close on quality names is not the risk that conventional wisdom suggests.

Does the overnight effect work for individual stocks?

Yes, though it varies significantly by stock quality and trend. Stocks with strong institutional interest, consistent upward momentum, and favorable RSI positioning tend to show the overnight effect most reliably. Highly speculative or downtrending stocks can gap down just as easily as up.

What is the best RSI level to buy a stock for overnight gains?

Looking for stocks that have dipped below RSI 30 and are beginning to recover is one of the cleaner setups. That oversold-to-recovery window — the run from RSI 30 to RSI 70 — is historically where overnight gap-ups cluster most densely.

What time of day do stocks gain the most?

Research suggests the bulk of gains occur in the overnight window from close to the next morning's open. Intraday — particularly the afternoon session — tends to be when noise trading dominates and net returns are flattest.